Gamuda ignites optimism

Over the years, Gamuda has been involved in infrastructure development and participated in the ownership of government awarded concessions of such projects.

However, given tariff pressures in both the water sector and also the tolled highway industry, it became clear that it was not a long-term sustainable business model to rely on government subsidies to maintain the contractual tariffs, as this has also became a financial burden to the government itself as it sought to preserve sanctity of contract.

This has been made all the more evident especially at a time when government finances have been pressured during the pandemic years and beyond.

As such, Gamuda elected to divest from those concession industries, being both water and tolled highways.

In the latest toll concession divestment, Gamuda ensured that the government also saved on its entire subsidy bill – totalling RM5bil as the ownership of the highways now rest with a not-for-profit entity called Amanat Lebuhraya Rakyat Bhd, thus ensuring toll rates do not increase and the concession duration remains as short as possible, and in some cases even shorter than the original concession duration awarded.That deal and the proceeds therefrom set Gamuda on a new pathway. While it had already ventured abroad prior to that, this time it decided to do so on a much larger scale, paving a way for overseas projects to contribute more significantly to its overall earnings.

As an example, for its last completed fiscal year ended July 31, 2022, overseas net earnings tripled to RM292mil year-on-year compared with the RM98mil in the previous year.

More notably, that RM292mil contribution made up 36.2% of the group’s overall net profit for the year, more than double the 16.6% of financial year 2021 (FY21).

Landmark London deal

Gamuda’s steadfast focus on international markets has thrust the company into the limelight this week. It announced it will be acquiring Winchester House (WH) in London, which is currently the United Kingdom’s headquarters of Deutsche Bank AG, in a 75:25 partnership with Castleforge Partners Ltd, a United Kingdom-based real estate private equity investor.

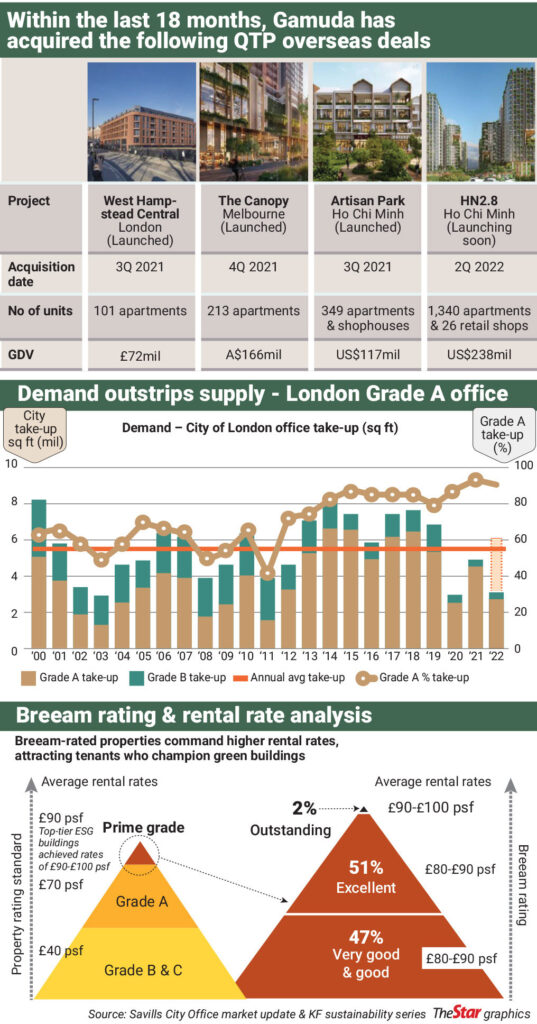

The deal is worth £257mil (US$317mil or RM1.4bil), and is the largest yet in the group’s Quick Turn-Around Project (QTP) strategy, which has seen Gamuda acquiring four properties in Vietnam, including the Dong Nai project, as well as The Canopy in Melbourne.

WH is a prime, well-connected commercial building located in the city cluster in the heart of London’s financial district, also known as the Square Mile.

To note, this is not the first London project for Gamuda. The group had back in in the third quarter of 2021 (3Q21) acquired the West Hampstead Central also as part of its QTP strategy, a project of 101 apartment units with a gross development value of £72mil (RM393mil).

But as Gamuda deputy group managing director Mohammed Rashdan Mohd Yusof says, the West Hampstead Central is just Gamuda “wetting its toes”, if compared to WH.

“First of all, the location of WH in the heart of London could not have been better, especially with the completion of the Elizabeth train line that effectively leads from where WH is to Heathrow airport,” he explains.

Rashdan tells StarBizweek, “Gamuda and our partner Castleforge, has commenced on the building approval via a pre-application process whereby it is a consultative and collaborative approach with the City of London council.

“We are highly cognisant that the city councillors know the vicinity best especially with respect to surrounding building application approvals too, and they have the best interest of the city and its occupants at heart.

In that regard, he says Gamuda will work closely with the city councillors to ensure the mutual objective of attracting the top global corporations and the best and brightest talent into the city is achieved.

“This will be done by providing top environmental, social and governance (ESG) Building Research Establishment Environmental Assessment Method (Breeam) ‘outstanding’-rated premises with future-proof and modern amenities, high quality finish, best-in-class facilities and beautiful design in WH’s soon-to-be newly refurbished offices, Rashdan reveals.

On the group’s partnership with Castleforge, he says the latter has the necessary expertise for just such a deal, that is to refurbish and upgrade a property to achieve a top Breeam rating of either “excellent” or “outstanding”.

“The fact they are already on their fourth managed fund, speaks volumes of the trust that their limited partners have of them in continuing their success.

“Therefore, we are pleased that we are partnering with them in this venture where we have 75% and they, through their fourth fund, have the remaining 25%,” says Rashdan.

In fund management and private equity, limited partners are partners that invest their money but are not involved with management of the fund, which is carried out by the general partner.

Rashdan is of the opinion that rental demand for office space in WH would be strong, especially if Gamuda has had the opportunity to carry out its refurbishment plans on the property.

Rationalising his optimism, he says, “London is seeing an ever-escalating demand for top-quality, ESG office buildings, and yet the supply of such prime assets is constrained, primarily due to the lack of building during the many years of Brexit uncertainty since 2016, exacerbated by the onset of the Covid years in 2020.

“There is also the difficulty of refurbishing older, non-ESG rated buildings given that they are currently tenanted. Many buildings in the city are also listed heritage buildings which further complicates the planning for refurbishments.”

These factors conspire to create a substantial supply bottleneck today which Gamuda in effect is capitalising on with the Winchester acquisition and business model, he says.

Interestingly, Rashdan adds the notable fact that Winchester House is not a listed building, and hence will be free of occupation shortly after the departure of Deutsche Bank to enable Gamuda’s planned refurbishment and upgrades.

As a number of analyst reports this week have revealed that a £149mil (RM813mil) of the £257mil (RM1.4bil) will be funded by a third party debt fund upon completion of the acquisition deal in approximately three months, Rashdan says on top the strong economic fundamentals of the deal, the funder was also highly comforted that the main backer for the acquisition is a Malaysian listed corporation, referring to Gamuda, with a clear track record in engineering, construction and real-estate developments. He adds, “Currently, we have a market capitalisation of approximately RM11bil, with a healthy and strong balance sheet with effectively no net gearing as at the end of October 2022, after the disposal of our highway assets for a total enterprise value of RM5.5bil.”

In terms of security, Rashdan notes that the debt funder has a first charge on the property as collateral and it is further assured that the interest servicing is covered by the rental payments of Deutsche Bank.

Industry analysts are also generally optimistic about the WH deal, with most of them maintaining a “positive” or “buy” call on Gamuda. Nomura Research’s Tushar Mohata and Alpa Aggarwal think the transaction could prove to be value accretive for the group overall.

“The funding terms are attractive with funding commitments very low in the initial years. We believe the key will be in minimising risks of below-expected rental rates.

“Another positive catalyst can be Gamuda managing to get a co-investor in this project, to reduce its funding requirements further,” says the duo in their research note.

Analyst for Macquarie Capital Securities Sdn Bhd Danial Razak sees Gamuda’s effort to convert the building into a Breeam-rated Grade A property as the right move, as it should double the rental rates of the building to £90 to £100 (RM492 to RM547) per sq ft, from the current £47 to £50 (RM257 to RM273) per sq ft, a rate that has more or less stagnated since 2012.

Meanwhile, Rashdan also reiterates Gamuda’s intentions to form a syndicate via equity partnership, effectively opening the door to third parties in the investment, citing the example of Gamuda possibly bringing its stake from 75%, down to 38%.

“This is just an illustration of course, but at 38% we would still have significant influence in the deal, although we would no longer hold the majority share. In fact, there are already several parties that have expressed keen interest to co-invest alongside us, and discussions with these potential investors are currently ongoing. Nonetheless, our priority is to complete the acquisition first,” he says.

On this specific plan to bring in a third party co-investor, Macquarie’s Danial believes it is part of Gamuda’s risk mitigation strategy given its exposure to other QTPs.

“By recognising future contributions at associate level, Gamuda will keep the debts from this acquisition off its books. Even if Gamuda fails to find a co-investor and its net gearing increases to 24% with that possibility, it is still well below the 70% internal gearing limit,” the analyst notes.However, appearing to provide a balanced perspective while acknowledging the investment as opportunistic, CLSA Research analyst Peter Kong says the WH project bears larger financial risk on a greater outlay if compared with Gamuda’s other QTPs, and involves gestation in refurbishing WH into a top sustainability-rated building.

On the other hand, concurring with Rashdan’s analysis that London possesses strong demand for sustainability-rated buildings, Kong says properties that are under the “outstanding” category in terms of Breeam ratings are normally fully leased within six months of obtaining the certificate of practical completion, quoting global real estate services firm Jones Lang LaSalle.

“This gives us confidence that there would be demand for properties with a high sustainable rating. Gamuda’s strategy is also to pre-lease 30% of its office space before practical completion to lock in rates,” he says.

Rashdan confirms that QTPs would be a strategy the group would be looking to embark on for Gamuda Land moving forward. Going a step further, he says Gamuda plans to diversify this QTP strategy geographically beyond Malaysia, with London being one of the main hunting grounds.

“We are looking at similar internal rate of return or better, for any potential contender for our QTP strategy. QTPs therefore, will generate a continuous pipeline of projects, which means as one project ends and divests, another starts with the capital being reinvested which will provide us consistent earnings growth and to do so with no new injection of capital either, as the proceeds of one project is reinvested into the next one,” he details.

Despite noting that township development remains Gamuda Land’s core business model, he says returns over the last decade or so have been challenging due to the combined double-whammy of eroding disposable incomes due to the worsening middle-income trap problem, which is affecting affordability, as well as much higher construction and compliance costs.

While acknowledging that this is a problem being faced by all property developers in Malaysia, Rashdan says Gamuda has chosen to tackle the issue head-on, consciously having crafted its QTP strategy to complement its township development model, in order to boost its overall real-estate return-on-capital employed.

“When combined with our leading engineering and construction business, with positive regional growth especially in Australia now, we have two strong core business engines in Gamuda Engineering and Gamuda Land to drive growth in profitability, and advancement in shareholder value, in the coming years,” he reflects.Prospects are certainly looking exciting for Gamuda both locally and abroad, as it is also widely anticipated to play another major role in the approved MRT3 project in the Klang Valley. This has also prompted Macquarie’s Danial to call the counter a marquee buy, a call which incidentally has also been issued by most research houses covering the company.